![]() Innovative Solutions. Proven Expertise.

REAL ESTATE MERCHANT BANKING

Innovative Solutions. Proven Expertise.

REAL ESTATE MERCHANT BANKING

Fed Delays Rate Increase Bringing Continued Stability and Low Rates To CRE

For the past several months, the commercial real estate industry has been awaiting the decision that would impact not only its bottom line, but also its momentum towards a stronger recovery. While labor markets have strengthened, downward pricing pressure from the decline in oil and commodities has kept inflation below the Federal Reserve’s target. In fact, the Fed took the path of least resistance and voted to keep interest rates at 0.25 percent as inflation remains below the two percent mark.

At the press conference following the Fed’s decision, Federal Reserve Chairwoman Janet Yellen echoed Stanley Fischer’s thoughts during the Jackson Hole Summit last month. Fischer explained that unemployment is not what’s slowing inflation. The lagging inflation is rather a product of a drop in oil and commodity prices, and a rise in the dollar. The strength of the dollar allows for cheaper imports but impedes exports. The Fed offered no insight in a recent press release as to the timing of the rate increase but will do so “when it has seen some further improvement in the labor market and is reasonably confident that inflation will move back to its 2 percent objective over the medium term,” according to the issued statement.

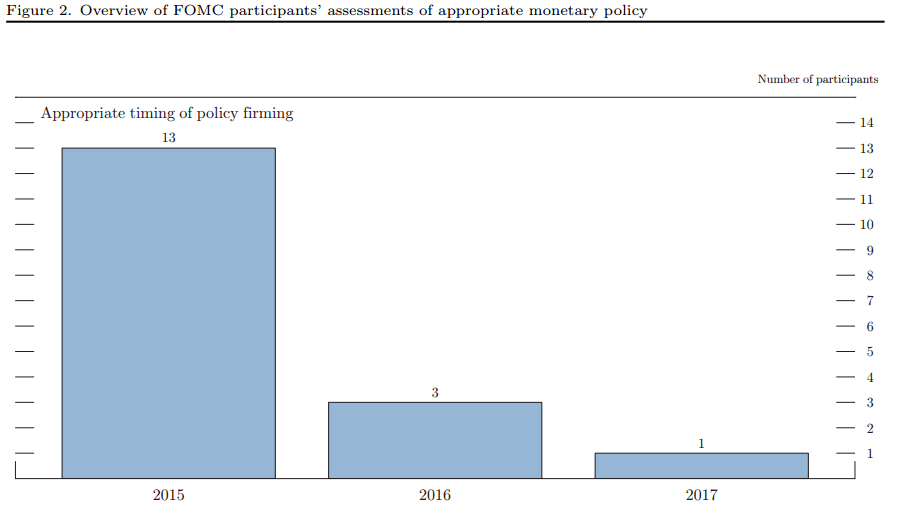

The 16-1 vote against raising rates today was the first time since January that Fed members were not unanimous in their voting. The decision will be tabled until their next meeting, where projections show 13 policy makers seeing higher rates by the year end. Based on the forecast, we are likely to see only one increase in October or December, down from two in the previous forecast.

The graph below was released in September and shows when FOMC participants find it appropriate to raise interest rates.

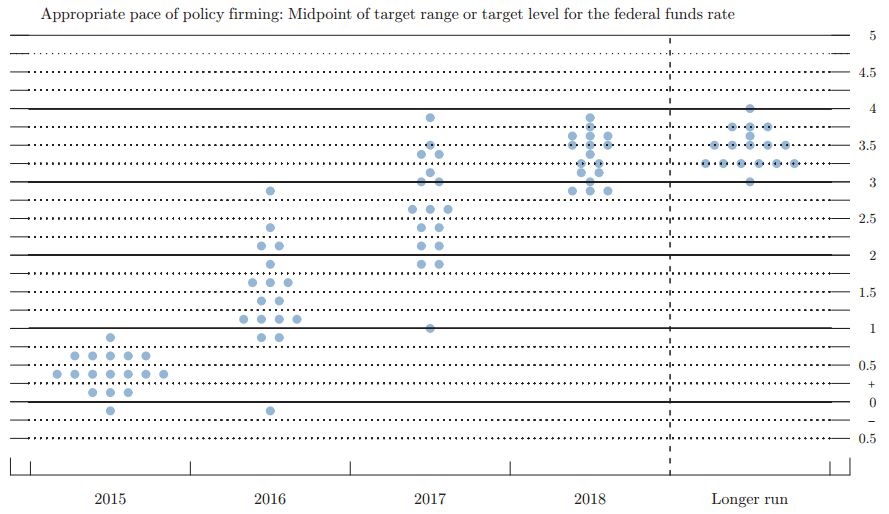

The Dot Plot below was released in September and shows where FOMC participants predict the federal funds rate to be. It is important to note that the dot plot is a tool that provides insight as to how the committee members felt at the September meeting.

What does this mean for commercial real estate? The Fed’s decision brings stability and continuation of low interest rates for construction, bridge, and floating rate loans. Additionally, the pressure on bank earnings net interest margin should encourage lenders to increase real estate lending.

♦

Dekel Capital at Western States CREF Conference

While at the Western States CREF Conference in Las Vegas, Dekel Capital saw an increase in new capital providers seeking to gain a toehold among the already competitive field of CMBS Lenders, Bridge Debt Funds, and Bank Lenders.

Non-recourse bridge lending on both cash flowing and non-cash flowing value-add plays is aggressively pricing in the high 4 percent’s to low 6 percent’s across all product types, at up to 80 percent of project costs. The market for non-recourse construction lending is also becoming more fluid at leverage up to 60 percent – 65 percent, as new players enter the space. The new “new money” at CREF was mezzanine debt at up to 85 percent LTV behind CMBS and Agency financing, fully co-terminus with the first TD. This mezz debt prices in the low double digits.

Lastly, banks are also expanding their lending programs, offering fixed rate loans that serve as lower cost options to CMBS and Agency debt, in some cases with more flexible pre-pay structures.