![]() Innovative Solutions. Proven Expertise.

REAL ESTATE MERCHANT BANKING

Innovative Solutions. Proven Expertise.

REAL ESTATE MERCHANT BANKING

The beginning of 2015 has been eventful for the real estate capital markets. While the jury is still out on what comes next, here are the top five indicators of what’s been and what’s coming:

GE Capital exits the lending business

In April of this year, GE exited the banking business by spinning off GE Capital, the higher risk $500 billion finance business that was 42 percent of company profit last year. The company has already sold $26.5 billion worth of office and CRE debt to Blackstone Group LP, Wells Fargo, and other investors, and is expected to fully divest as early as 2016. Part of the $9 billion portfolio Wells Fargo purchased from GE Capital included loans for manufactured homes and communities, a space dominated by Wells Fargo ($7 billion in loans since 2004) and GE Capital ($6.2 billion loans since 2004). Now, as the clear leader in manufactured home lending, Wells Fargo plans to expand the division and has recently hired Matt Krasinksi and Lew Grace, two GE Capital veterans, to lead the charge. Other lenders have been working towards capturing the $10 billion GE was originating per year of both bridge and permanent loans.

Fannie and Freddie shift gears after high production volume in Q1 and Q2

Also in April, Fannie Mae and Freddie Mac slowed down their multifamily lending program because both government sponsored enterprises were on track to exceed their annual limit of $30 billion each by Q3 2015. The annual lending caps, which only apply to market rate apartment loans, were established in 2013 by the Federal Housing Finance Agency to encourage more private capital in the market. Fannie Mae issued $10.4 billion in Q1 and $14.5 billion during Q2 in multifamily mortgage-backed securities, while Freddie Mac’s multifamily lending volume hit $10 billion for Q1 and $13.1 billion for Q2. This high production volume has been driven by low interest rates, large loan sizes and overall higher demand for apartments as well as deferred business from the end of 2014.

Fannie and Freddie slowed down process by tightening their underwriting and increasing spreads. Currently their focus is on “affordable housing” and properties under 100 units, both of which are excluded from the cap.

Basel III’s impact on construction lending

BASEL III is a global bank framework that proposes further banking regulation on capital adequacy, stress testing and market liquidity risk. Basel III was created in an effort to repair the financial crash and restore a proper financial system. It forces banks to hold substantially more capital, or shrink their footprint, which reduces the effect they would have on the financial system if they were to fail.

The overall significance of Basel III is that with banks improving their capital ratios, there will be less liquidity in our global capital system. Because of this, smaller or weaker banks might find it difficult to raise capital, which could ultimately result in banks exiting the market place, merging or being acquired.

High Volatility Commercial Real Estate: Under Basel III, regulators created this new category which applies to acquisition, development and construction loans requiring higher capital reserves. This is making these loans more expensive for banks to fund. Furthermore, the new rules require a 15 percent minimum cash equity requirement to avoid a High Volatility designation, as well as max 80 percent LTV on the finished product. Specifically, the appreciated value of the land does not count towards the equity requirement, only the cash paid for the land or the original basis.

Global economy slows, the outlook on short-term rates

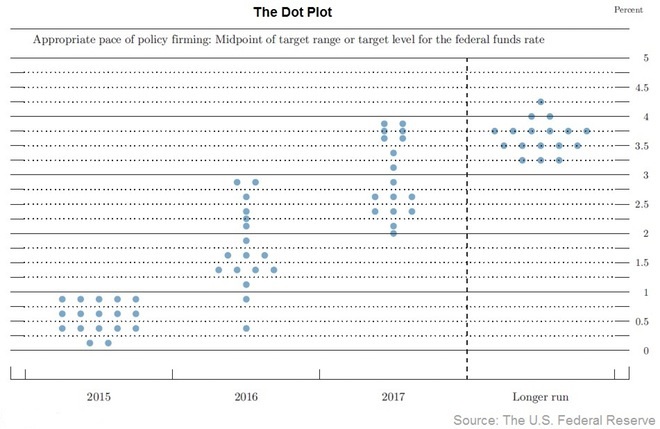

The recent free-fall of the Chinese financial markets created some of the worst volatility in our capital markets since 2009. This market volatility has scared investors, which resulted in a flight to safety, causing the 10-year treasury to drop below 2% for the first time since April of this year, compressing the treasury yield 20 basis points in the past week. The global economic slowdown will cause the Federal Reserve unanticipated aggravation leading up to their September 17th meeting. In light of this, the overwhelming market expectations that the Fed would start raising rates in September is becoming more of a 50/50 proposition.

The Dot Plot below was released in June and shows where each Fed member predicted federal funds rate to be. It is important to note that the plot is not official, but rather a tool that provides insight as to how the committee members felt at their June meeting.

New lending sources bridge the divide for needed financing

New lending sources have entered the market to fill the gap as both banks and agencies face the lending hurdles described above. “Stretch senior” lending programs provide bridge loans up to 75 percent to 80 percent of cost for value-add repositioning of existing assets. Specific groups with dry powder are focused on medical office, creative office and multifamily. Mezzanine and Preferred Equity providers are showing an appetite in coming in behind these bridge lenders and pushing leverage up to 90 percent of cost. In a bid-to-win business, these mezzanine and preferred equity groups are lowering their minimum amount to $1 million in some cases. Lastly, various bank lenders are aiming to fill the capacity left by the agencies by offering attractive long-term, fixed rate, non-recourse loans.

♦

As we enter into the second half of 2015, it is important to note that there are disruptive market movements on the horizon. Clearly a change in interest rates will have a major impact, and with the regulatory environment in its current state, new lending sources will most likely continue to enter the market in order to bridge the gap left by banks and agencies. 2015 is shaping up to be an interesting year.