![]() Innovative Solutions. Proven Expertise.

REAL ESTATE MERCHANT BANKING

Innovative Solutions. Proven Expertise.

REAL ESTATE MERCHANT BANKING

As we reach the midpoint of 2017 with the 2016 presidential election now behind us, it seems like the “end of the current real estate cycle” has become a focus point for many of our investor/developer clients and capital providers. This industrywide focus on the “end” along with changing government mandates and market fundamentals may cause this cycle to extend beyond the “norm.”

Earlier this month we attended the ULI Spring Conference in Seattle, where the sentiment amongst conference attendees was heavily weighted towards the notion that we are in the later stages of the current real estate cycle. In light of this, the nature of the cycle discussion with investors, developers, and capital alike has been focused around risk exposure, protection of profits made so far in the cycle, and concern over new deals that might be exposed to the next downturn. For investors, this translates into acquiring assets with strong, predictable cash flow in more liquid primary and large secondary markets. For capital market participants, credit now rules the day, with more stringent underwriting parameters, as well as a focus on investing in or lending on projects that have less execution and market risk.

In addition to the cautious sentiment of market participants, we are seeing changes in government mandates and market fundamentals that are constraining new supply to the market. Recent changes to immigration and trade policies have helped drive up construction costs and prolong construction schedules by exacerbating labor shortages in the subcontractor trades and raising material costs.

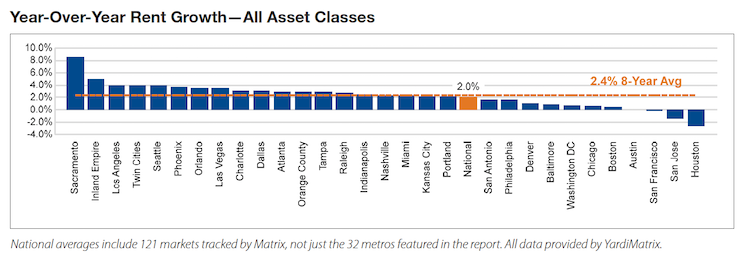

In the multifamily sector, record deliveries of new supply have abated rent growth in major markets throughout the country. According to a recent report by Yardi Matrix, multifamily rents were up 2.0% nationwide in April, down 50 basis points from March and well below the 5.5% growth rate of a year ago. The combination of increased costs, longer construction schedules and abated rent growth are lowering return metrics thereby making the deals less appealing to developers and capital alike.

Contrary to the latter part of the last cycle, where many felt that market cycles were a thing of the past and excessive risk and leverage were the norm, the recent pullback by investors and capital combined with the changes in government mandates and market fundamentals leads us to believe that the current market cycle will extend beyond the norm. This should present some interesting investment opportunities for the contrarian investors in the market.